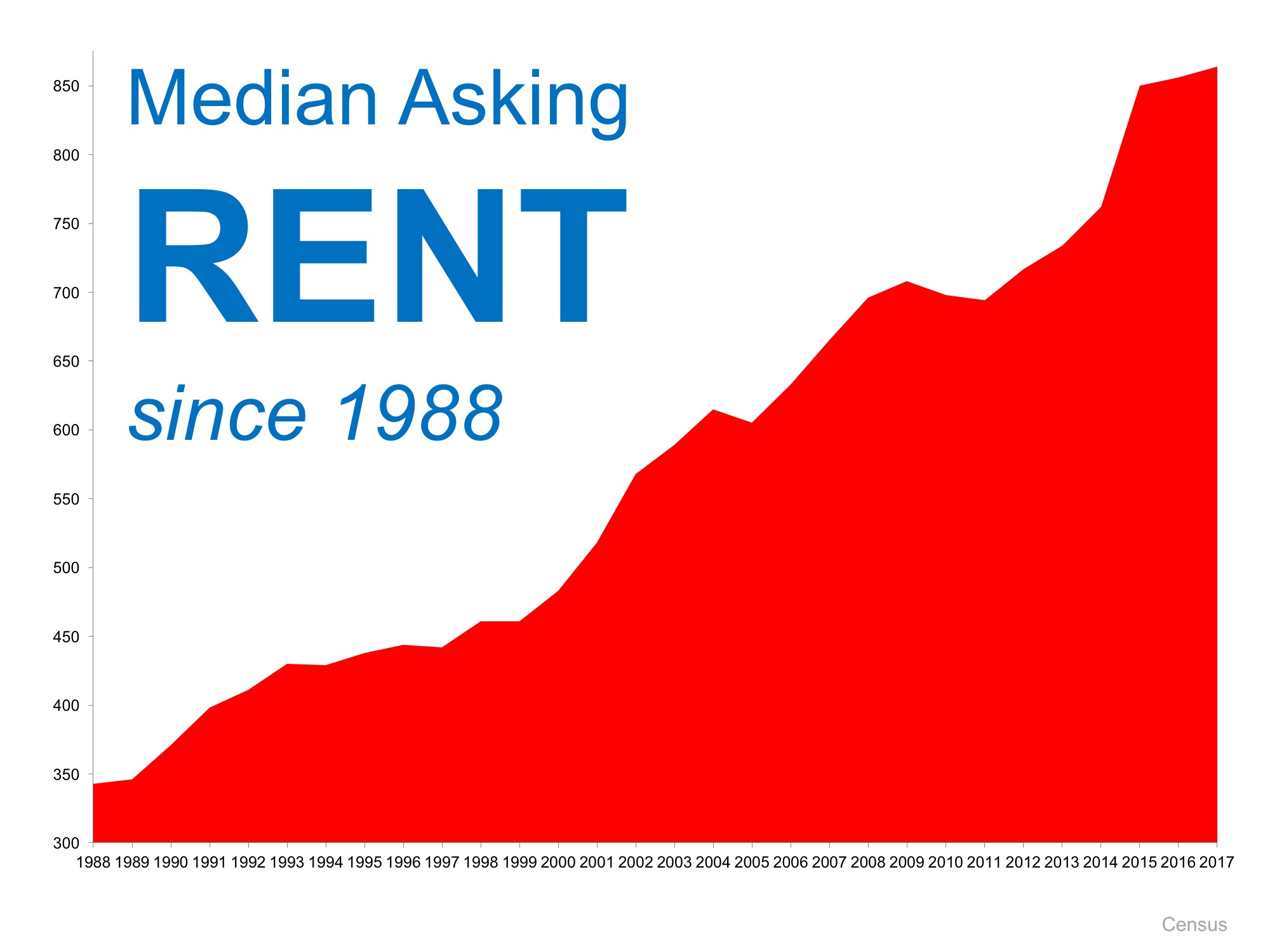

If you’ve entered the real estate market, as a buyer or a seller, you’ve inevitably heard the real estate mantra, “location, location, location” in reference to how identical homes can increase or decrease in value due to where they’re located. Well, a new survey shows that when it comes to choosing a real estate agent, the millennial generation’s mantra is, “local, local, local.”

CentSai, a financial wellness online community, recently surveyed over 2,000 millennials (ages 18-34) and found that 75% of respondents would use a local real estate agent over an online agent, and 71% would choose a local lender.

Survey respondents cited many reasons for their choice to go local, “including personal touch & handholding, longstanding relationships, local knowledge, and amount of hassle.”

Doria Lavagnino, Cofounder & President of CentSai had this to say:

“We were surprised to learn that online providers are not yet as big a disruptor in this sector as we first thought, despite purported cost savings. We found that millennials place a high value on the personal touch and knowledge of a local agent. Buying a home for the first time is daunting, and working with a local agent—particularly an agent referred by a parent or friend—could provide peace of mind.”

The findings of the CentSai survey are consistent with the Consumer Housing Trends Study, which found that millennials prefer a more hands-on approach to their real estate experience:

“While older generations rely on real estate agents for information and expertise, Millennials expect real estate agents to become trusted advisers and strategic partners.”

When it comes to choosing an agent, millennials and other generations share their top priority: the sense that an agent is trustworthy and responsive to their needs.

That said, technology still plays a huge role in the real estate process. According to the National Association of Realtors, 95% of home buyers look for prospective homes and neighborhoods online, and 91% also said they would use an online site or mobile app to research homes they might consider purchasing.

Bottom Line

Many wondered if this tech-savvy generation would prefer to work with an online agent or lender, but more and more studies show that when it comes to real estate, millennials want someone they can trust, someone who knows the neighborhood they want to move into, leading them through the entire experience.